VAT gap – missing VAT revenue within EU by companies who do not act in line with the local law, has been a challenge for many years. How would you manage to push foreign companies being resident on other continent without any physical presence in the country not caring about the law to register locally for VAT and pay whatever the government should get. This is quite difficult question and to find a pragmatical way which does not cost millions on control framework is not as easy.

The new e-commerce VAT package to come into force on 1 January 2021 in the EU seems to be the pragmatical solution governments might be looking for however the complexity might increase significantly. The aim of this e-commerce VAT package is to ensure complete and correct taxation in the destination state.

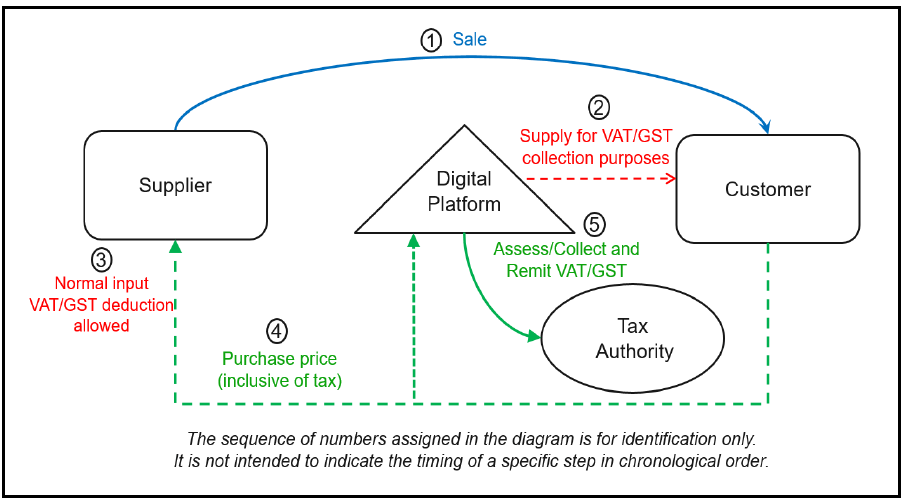

The biggest burden will be put on electronic interfaces (such as marketplaces, platforms, portals or other similar means) which will be liable for collecting and paying the VAT due on the supplies made by non-EU businesses to EU consumers facilitated through their platforms. In other words, the following fiction will be put in place: the electronic interfaces will be deemed to purchase the goods from the non-EU businesses and to sell them to the EU consumers.

In December 2019 (two years after the first legislative provisions on the e-commerce VAT package were published), the European Council adopted two legislative acts with new provisions for the e-commerce.

These new provisions clarify various aspects, such as the ones included below:

- Electronic interfaces are facilitating supplies and thus will be bond to the new rules when they allow a customer and a supplier to enter into contact, resulting in a supply of goods through their platform. This does not apply however if the electronic interfaces are not directly or indirectly involved in:

- setting the general terms and conditions of supplies;

- charging the payment to the customers; and

- ordering or delivering the supplies.

- Electronic interfaces are not considered to facilitate the supplies and thus not subject to the new 2021 rules if they:

- only provide payment processing services,

- list or advertise the goods or

- redirect customers to other electronic interfaces where goods can be purchased, without further intervention in the supply.

- To avoid any VAT non-payment risk towards the tax authorities, the transaction between the non-EU supplier and the electronic interface will be VAT exempt with credit, allowing the supplier to deduct the input VAT incurred on the respective goods.

- The transport of the goods will be allocated on the transaction between the electronic interface and the EU consumer.

- VAT on the supplies to the EU consumer will be due by the electronic interface when the payment confirmation, authorization message or a commitment for payment from the EU consumer is received (whichever earliest) and thus not postponed to a later stage when the payment is cashed.

- The electronic interfaces should not be held liable for any additional VAT resulted from the incorrect data provided by the suppliers if they can prove that they did not know or could not reasonably have known that the information received was inaccurate.

- Specific records would need to be kept by the electronic interfaces for the supplies performed through their platforms.

Source: OECD – The Role of Digital Platforms in the Collection of VAT/GST on Online Sales (March 2019)

The new rules bring major complexity into the day-to-day business of electronic interfaces, adding more responsibilities starting with 2021.

Preparing for implementing the new e-commerce rules should start with the assessment of the transactions performed and impact of the new rules and subsequently with various amendments to the ERP systems, transactions’ mapping, transport allocation changes, internal and external procedures, terms and conditions with both suppliers and customers, tracking and record keeping mechanisms to comply with the new e-commerce regulations.

As the responsibility with collecting VAT on the supplies performed through the platforms will be in the hands of the electronic interface, “know your supplier” procedures should also be put in place or revised to ensure a proper functioning of the business. This might be administratively demanding task.

While 2021 might seem quite far away, complying with the e-commerce rules will require many dedicated resources.

For further information please see the attached links or contact the following persons:

Andras Salanki, andras.salanki@ch.pwc.com,

Andreea Dereli, andreea.d.dereli@ch.pwc.com

Image Source: http://unsplash.com

[…] Source Mihaela Merz […]

LikeLike

[…] Source: michaelamerz.org […]

LikeLike