In brief

October 1, 2019 saw major changes come into effect with regard to the Japanese Consumption Tax (“JCT”) regime, which for the first time introduced multiple tax rates (8% and 10%). Additionally, with effect from October 1, 2023, the JCT rules introduce a new qualified invoice regime, under which a purchaser will only be able to obtain a JCT input credit if presented with a qualified invoice. During a transitional period from October 1, 2019 until the new qualified invoice rules come into effect, stricter JCT invoice and bookkeeping rules apply, requiring taxpayers to include more detailed information in their invoices and books. It will also be necessary for all taxpayers wishing to issue “qualified invoices” to register with Japan’s National Tax Agency (“NTA”) prior to October 2023. In short, Japan’s JCT regime has become increasingly complex. In order to ensure proper compliance, it is essential that taxpayers understand not only the current rules, but also the transitional provisions and the rules coming into effect going forward, to allow sufficient time to timely register, and to amend accounting software and properly train relevant personnel if necessary.

In detail

1. Summary of Amendments

Japan’s Diet promulgated certain changes to the JCT rules through the 2016 tax act (“2016 tax act”, which amended the 2012 tax reform act with the objective of ensuring stable tax revenue). Certain changes, including the introduction of multiple rates, came into effect on October 1, 2019; other changes will come into effect going forward, as discussed below.

The JCT-related measures in the 2016 act are as follows: (i) increase the headline consumption tax rate to 10%, effective October 1, 2019, (ii) a new reduced tax rate system, applicable to certain foods and newspapers, effective October 1, 2019, (iii) a new invoicing system, effective October 1, 2023 (iv) a new “Transitional Invoice Retention System”, effective from October 1, 2019 until September 30, 2023, (v) special rules regarding eligibility for an input tax credit when making purchases from JCT exempt entities, and (vi) changes to the calculation method for input and output tax, applicable to small and medium-sized corporations. A general timeline of the new JCT rules is shown as below.

2. Determining Applicable Tax Rate for Transactions Straddling the Effective Date of the New Tax Rate Rules (October 1, 2019)

Any taxable transaction carried out on or after October 1, 2019 will be subject to the new tax rate of 10%, or 8% for certain transactions eligible for the reduced rate. Transactions subject to the general rules include transfers of assets, leasing of assets, provision of services within Japan, provision of electronic services from offshore to a Japanese resident, or import of goods. The applicable tax rate will generally depend on the actual transaction date, without regard to the contracting date or date of payment.

The transaction date will depend on the transaction type. A transfer of assets, the provision of services, or import of goods, which straddles the October 1, 2019 effective date should as a rule be treated as follows.

- Output tax and input tax in an inventory sale occurring on or after October 1, 2019. The output tax on a sale of inventory taking place on or after October 1, 2019 should apply the rate applicable under the new tax rate rules. The applicable input tax credit rate will depend on when the inventory was purchased; if purchased before October 1, 2019, the input tax credit should be calculated based on the old rate (8%), even if the purchaser sells the inventory on or after October 1, 2019.

- Applicable tax rate for a service commenced prior to effective date of rate increase. The transaction date for purposes of the provision of a service is the completion date of the entire service, as agreed upon in the contract, or the date that the service provider hands over any deliverable it had agreed to deliver to the service recipient. Therefore, if the parties agreed before October 1, 2019 to provide services for a one-year period ending on or after October 1, 2019, and made a lump sum payment on the contract date, the whole service should be subject to the new tax rate. As an exception, if the payment is non-refundable and the vendor (based on its normal practice) booked the whole amount as service income on the date of receipt, the old rate may apply.

- Regularly provided services. Where a service is by nature one that is provided regularly (for example, regular monthly floor cleaning, regular machinery maintenance, etc.), the applicable rate will depend on the month that the service is provided. The old rate would thus apply to regular services provided before October 1, 2019, and the new rate would apply to such services provided on or after October 1, 2019.

- Import of goods. Imported goods are subject to JCT when carried out of a bonded area. Therefore, for imported goods carried out of a bonded area on or after October 1, 2019, the new rate will apply.

Transactions other than those subject to the general rules are subject to specific transitional rules, details of which can be found here >

3. Introduction of Multiple Tax Rates and Transitional Invoice Retention System

Certain transactions will continue to be subject to the reduced 8% tax rate, regardless of the general tax rate hike from 8% to 10% effective October 1, 2019. The reduced rate will apply to the sale of (1) food and beverages defined in the Article 2 of the Food Labelling Act (excluding alcoholic beverages), including both B2C and B2B transactions, and (2) newspaper subscriptions, for papers issued at least twice weekly.

Some complexity exists with regard to determining the applicable tax rate with regard to food-related services. The law treats the sale of food to diners at restaurants, and the provision of catering services, to be a “provision of services”, rather than “a sale of food”, such that the 10% tax rate, which is generally applicable to services, applies. The taking out of food from a restaurant or home delivery of food are considered the sale of food and beverages, however, and are thus subject to the 8% reduced rate.

Despite the seeming simplicity of the above definition however, many complexities apply. For example, certain B2B transactions may be difficult to judge the applicable tax rate. Even if the final products are not food or beverages, the selling of food and beverage raw materials would be subject to the 8% tax rate, because the sales method is not relevant for judgement of the applicable tax rate. Examples of some of the complexities are provided in Q&A prepared by the NTA, as summarised in the table below.

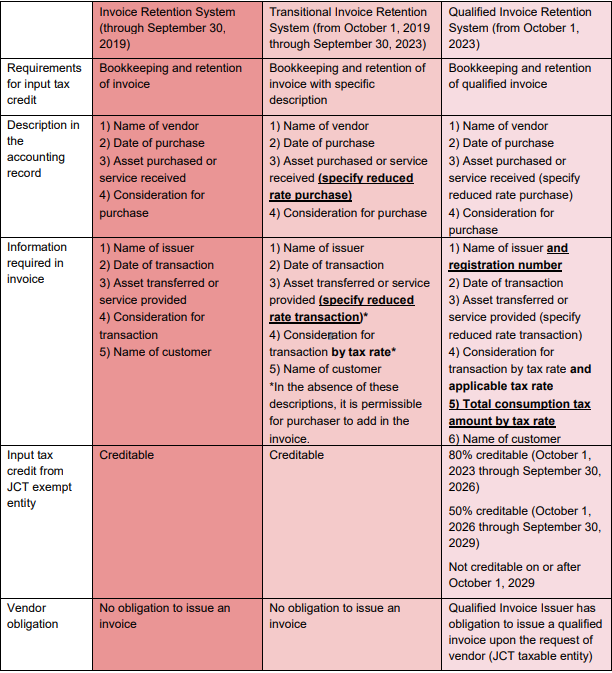

The Transitional Invoice Retention System applies during the four-year period beginning October 1, 2019 and continues until the Qualified Invoicing System comes into effect on October 1, 2023. Under the Transitional Invoice Retention System, invoices must specify the sales amount and the applicable tax rate. Correspondingly, taxable purchases must be recorded in the taxpayer’s books at the applicable tax rate in order to claim an input tax credit.

Under the Transitional Invoice Retention System, it is necessary for a taxpayer to classify its general expenses at either the 8% or 10% JCT rate for bookkeeping purposes, depending on the effective rate as at the date the expense arose. Thus, any business entity, regardless of whether it expects sales of reduced rate products, should modify its accounting system to cope with multiple tax rates, in order to be able to claim an input tax credit on its JCT returns.

In addition, merely noting in the books that a transaction is subject to an 8% rate will be insufficient. Considering requirements for preparation of JCT returns, it will be necessary to distinguish between transactions eligible for the (new) reduced 8% rate versus those subject to the (old) headline JCT rate of 8%, due to a different allocation between the national and local JCT portions in the new and old 8% rates.

4. Changes in Input Tax Credit Requirements

Under both the Transitional Invoice Retention System (effective up to October 1, 2023) and the Qualified Invoice Retention System (effective from October 1, 2023) a taxpayer is required to comply with relevant bookkeeping and invoice retention requirements in order to be eligible for an input tax credit. The information required to be included in invoices and for bookkeeping purposes differs from what was required prior to October 1, 2019.

Under the Transitional Invoice Retention System, a taxpayer may potentially obtain an input tax credit with respect to taxable purchases from any vendor, regardless of whether such vendor is a JCT taxable entity or a JCT exempt entity, if the taxpayer obtains a JCT compliant invoice. On the other hand, going forward under the Qualified Invoice Retention System, a taxpayer will only be eligible for an input tax credit, assuming other requirements are met, with respect to a purchase from a JCT registered vendor. Additionally, the Transitional Invoice System applies certain additional requirements with regard to obtaining an input tax credit, effective until September 30, 2029. Essentially, a taxpayer’s ability to obtain an input tax credit with regard to a purchase from a vendor that is a tax exempt entity is phased out.

A summary of the applicable rules under the different regimes appears in the table below.

Thus, as summarized above, from October 1, 2023 it will be essential for a purchaser to confirm that an invoice is a Qualified Invoice (with a JCT registration number) received from a Qualified Invoice Issuer, in order to ensure that the purchase is eligible for an input tax credit.

5. Registration of Qualified Invoice Issuer

It will be necessary for vendors to register with the NTA in order to be able to issue a Qualified Invoice. A JCT exempt entity will be ineligible to register as a registered entity. Application for registration begins on October 1, 2021, and in order to become a registrant by October 1, 2023, the vendor should file the application with the relevant local tax office no later than March 31, 2023.

The NTA will publish a list of registered entities on its website. The list should show the name of registered entity, the location of its head office, the entity’s registration number, and the date of the registration.

6. Takeaways

Changes to the JCT regime should affect both Japanese and foreign corporations that engage in JCT taxable transaction in Japan. Under the Transitional Invoice Retention System (effective from October 1, 2019 through September 30, 2023), it is necessary to ensure that customer invoices satisfy statutory requirements. For input tax credit purposes, it is critical that taxpayers’ accounting and bookkeeping systems are properly adjusted to deal with the multiple tax rate system. Further, in order to be prepared for the upcoming Qualified Invoice System, it will be critical for taxpayers to review their current accounting systems, and possibly train their accounting division personnel to be able to comply with the new rules, and to timely register in order to issue Qualified Invoices.

For further information contact PwC Tax Japan

Email: pwcjapan.taxpr@jp.pwc.com

Image source: Unsplash.com

[…] Source Michaela Merz […]

LikeLike