On 19 July 2019, the changes in the Polish VAT law have been approved and published.

On 19 July 2019, the changes in the Polish VAT law have been approved and published.

One of those revolutionary changes relates to the implementation of the Mandatory Split Payment Mechanism as of 1 November 2019.

The main purpose of proposed changes is to:

- replace the currently existing mechanism (i.e. domestic reverse-charge) with the Mandatory Split Payment Mechanism; and

- implement changes in connection with rules regarding tax liability (i.e. liabilities of parties involved in the Split Payment Mechanism in Poland).

The scope of the regime:

- When?

1 November 2019

- Who?

VAT-registered, including non-resident companies

- What?

B2B domestic Transactions with the gross value of and above PLN 15’000.00 (EUR 3’505)

The Mandatory form of the regime will be applicable for supplies of goods and services, which are currently covered by the domestic reverse-charge regime.

Additionally, it is proposed to include also transactions involving parts and accessories for motor vehicles; coal and coal products; electrical machine and devices, their parts and accessories, electrical devices, their parts and accessories.

A detailed list of goods and services covered by the regime is included in the attachment 15 of the bill.

- Cash or credit card?

Only bank transfers

- Penalties

30% of the VAT amount due on the invoice / transactions with no reference to the Mandatory Split Payment Mechanism (i.e. joint liability of the supplier as well as the recipient to verify the correctness of the invoice issued/received under the Mandatory Split Payment Mechanism; e.g. no transparent note on the invoice, whether goods/services are in-scope of the regime) or can result with the penalty up to 720 daily rates.

Additionally, if the recipient has not aid for goods and services using the regime, he cannot classify the purchase, as an overall cost of the business from direct tax point of view (e.g. cost of goods sold).

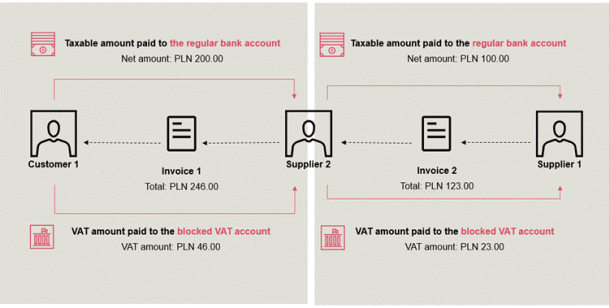

- Blocked VAT Account

Amount gathered on the blocked VAT account can be withdrawn for other purposes other VAT payment (e.g. payment of other tax liabilities)

- Invoicing

It is proposed that invoices should include a special indication “mechanism podzielonej płatności” (ENG. “split payment mechanism”)

- Bank account for foreign entities

The obligation to have a regular bank account and the blocked VAT account in Poland in connection with transactions subject to the regime (Also for VAT-registered foreign taxpayers).

Main areas of goods and services that will be affected by the regime (based on the attachment 15 of the Polish VAT law, which includes the full list of goods and services):

- Steel products, precious metals, non-ferrous metals;

- Waste, scrap, recyclable materials;

- Electronics, specifically: processors, smartphones, phones tablets, net-books, laptops, game consoles, inks, toners, hard drives;

- Fuels for cars, fuel and lubricating oils

- Greenhouse gas emission rights;

- Building and construction services;

- Coal

- Sale of car and motorcycle parts;

Should you have any additional questions, please contact:

Zsolt Tenczer, Senior Manager

Tel. +41 58 792 45 60

E-Mail: zsolt.x.tenczer@ch.pwc.com

Kinga Zawora, VAT Senior

Tel. +41 79 339 98 95

E-Mail: kinga.x.zawora@ch.pwc.com

Image source: unsplash.com

[…] Source Michaela Merz […]

LikeLike