Even if the Swiss VAT law is quite similar to the principles implemented into the EU VAT law, there are some important differences which often confuse foreign companies doing business in Switzerland.

One of the main reasons for confusion is the definition of goods in Switzerland as it differs quite a lot from the definition known from the EU VAT law.

According to the Swiss VAT law, goods and the supply of goods are defined as follows:

Art. 3 Definitions

In this Act:

b. Goods means movable and immovable objects and electricity, gas, heating, refrigeration and the like;

c. Supply means the concession of a usable economic asset to a third party in expectation of a consideration, even if it is required by law or based on an official order;

d. Supply of goods means

1. the transfer of the power to dispose of a good commercially in one’s own name,

2. the delivery of a good on which work has been performed, even if the good is not altered by the work, but only tested, calibrated, regulated, checked for its function or has been treated in another way,

3. making a good available for use or exploitation;

Therefore the place of supply differ as well from what professionals trained on EU VAT law would expect to be the place of supply:

Art. 7 Place of supply of goods

1 The place of supply of goods is the place where:

a. the good is located at the time of transfer of the power to dispose commercially of it, of its delivery or of its being made available for use or exploitation;

b. the transport or dispatch of the good to the customer or to a third party on his instructions begins.

Especially in global contracts between two non Swiss resident entities where their Swiss resident group companies are involved in delivery, mistakes in determination of place of supply occur quite often. This leads to wrong VAT treatment even of the transaction and can go as far as even failing to recognize the foreign entities would need to register for Swiss VAT purposes. As this mistake can be quite costly, correct analysis and implementation of global agreements is an absolute must for Swiss VAT purposes.

Please see below a small case study of a mistake that happens quite frequently.

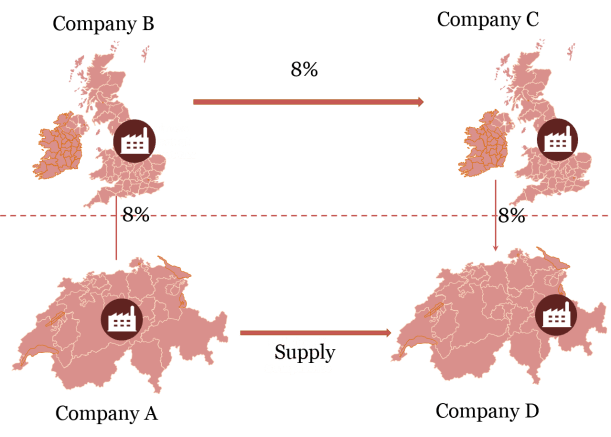

Background

The supplier, Company B, which is located in an EU member state, entered into a global framework agreement for IT outsourcing services in a wide sense with its client (Company C), also located in an EU member state.

Under the respective outsourcing agreement, leasing of hardware and hardware maintenance in connection with electronic workplace services are offered. The leasing and maintenance services are provided in Switzerland by the Swiss subsidiary (Company A) of Company B in favour of the Swiss subsidiary (Company D) of Company C. Leasing and maintenance of hardware is defined as supply of goods according the Swiss VAT Law, which means the place of supply for these “services” is in Switzerland and subject to 8% Swiss VAT.

What does this mean for the allocation of the costs between these companies?

As the leasing and maintenance services take place in Switzerland, the electronic workplace services have to be invoiced from the Swiss entity (Company A) to the EU based entity (Company B) with Swiss VAT of 8%. If Company B annually invoices more than CHF 100’000 of these services to Company C, Company B will have to register for Swiss VAT and charge 8% Swiss VAT to Company C. If the EU-based Company C then on-charges more than CHF 100’000 annually to its Swiss subsidiary, it will also have to VAT register in Switzerland and charge 8% Swiss VAT to the Swiss subsidiary.

The situation can be graphically presented as follows:

Swiss VAT consequences and solutions

Swiss VAT consequences and solutions

Crossing the threshold for registration leads in such a business set up to two additional VAT registrations in Switzerland. The easiest option to avoid VAT registrations and administrative cost will be to arrange that costs are directly charged between both Swiss domiciled entities without involvement in the recharging of the cost of the foreign companies.

If this should not be possible or desired, the Swiss VAT consequences need to be determined on the basis of the current Swiss VAT regulations.

On this basis, strict turnover thresholds determine potential VAT registration obligations in Switzerland.

In case the annual taxable turnover in Switzerland amounts to CHF 100’000 or higher, companies are required to register for Swiss VAT. The place of establishment of a company is not relevant for the determination of an obligation to register for VAT from a Swiss point of view.

Even if invoices are issued outside of Switzerland for the purpose of on-charging supplies, the place of delivery according to Swiss VAT law is deemed to be in Switzerland. This concerns both, the leasing as well as the hardware maintenance services. The Swiss VAT registration obligation results for the non Swiss contracting entities as well.

Only if all companies in the chain are registered for Swiss VAT, it will be possible to deduct input VAT. Otherwise, the input VAT cannot be deducted and will at one point constitute final costs.

What does it mean if you do not act in line with the law?

The companies will be penalised and will have to pay late payment interests and against the management criminal proceeding might be opened if found by the Swiss Tax Authority.

Future legislation

Even if you think that these requirements may not affect you because you do not reach the turnover threshold in Switzerland, you should read the following sentences carefully. It is currently being discussed to amend current threshold regulation in the Swiss VAT law. The legislation should be adapted in the way that in case a turnover of CHF 100’000 worldwide is achieved, a Swiss VAT registration is triggered by any supply of goods (and certain services) in Switzerland.

Therefore, Swiss VAT registration obligations may result already after just one Swiss Franc of turnover in Switzerland is achieved annually.

Currently, it is assumed that the new legislation may come into effect as from 1 January 2018.

Therefore, if you do business in Switzerland, you should keep this development in mind and carefully consider the consequences.