![]() Introduction of the so called “European VAT group”

Introduction of the so called “European VAT group”

The Budget Law 2017 has introduced, in the Presidential Decree no. 633/1972, the new title V-bis which regulates the institute of the VAT group, effective from January 1, 2018, subject to prior consultation of the European VAT committee.

The VAT group will be, actually, in force:

- starting from January 1, 2019, whether the declaration in order to elect the option is submitted between January 1, 2018 and September 30, 2018;

- starting from January 1, 2020, whether the declaration in order to elect the option is submitted between October 1, 2018 and December 31, 2018.

The option would be binding at least for a period of 3 years and remains valid for every year following those 3 years until it is revoked (on the basis of the new article 70nonies, Presidential Decree no. 633/1972), except for the cases, properly regulated, of the end of the VAT group ex lege.

In brief, taxable persons established in the Italy carrying out business or professional activities, for which financial, economic and organizational links are met, can be treated as one single taxable person, identified with just one VAT number.

In the case of election of the VAT Group:

- transactions between taxable persons participating to the VAT group are considered as not relevant for VAT purposes;

- the VAT group operates as single VAT taxable person towards those not participating the group itself.

The new rules would represent the implementation of art. 11, EU Directive no. 2006/112/EC, according to which “After consulting the advisory committee on value added tax (…), each Member State may regard as a single taxable person any persons established in the territory of that Member State who, while legally independent, are closely bound to one another by financial, economic and organizational links”. As above indicated the new regime, provided by the Budget Law 2017, is optional. Having said that, if the requirements provided by the law in order to elect the option are met; the option, where elected, should be exercised for all subjects which meet these requirements (so called “all in, all out principle”) and it would be an alternative to the so-called “VAT group settlement” provided by article 73, paragraph 3, Presidential Decree no. 633/1972 (also subject to changes, starting from January 1, 2017; please see the following paragraph).

For further details of the main aspects of the European VAT group, please click HERE.

Changes to article 73, paragraph 3, Presidential Decree no. 633/1972, so called “VAT group settlement regime”

The Budget Law has replaced the text of the paragraph 3 of article 73, Presidential Decree no. 633/1972, regulating the so called “VAT group settlement regime”.

The new paragraph is applicable starting from January 1, 2017. However, the Budget Law refers to a Decree of the Minister of Economy and Finance in order to adjust the current ministerial regulations to the changes introduced.

On the basis of the new text:

- it is no longer mandatory for the controlling company to submit the VAT returns of the controlled companies to the Italian tax authorities’ office of the fiscal domicile of the controlling company itself;

- as clarified in the Government’s report to the draft Budget Law 2017, it is stated that not only share capital companies, but also partnerships and other entities that are taxable persons can opt for the VAT group settlement regime, both as controlling company and as controlled company;

- the entity or “controlling commercial company” communicates to the Italian tax authorities the exercise of the option for the VAT Group settlement regime “via the annual VAT return submitted starting from the year in which the controlling company intends to elect the option”. The entity or controlling company which, meeting the requirements, intends to exercise the option for the regime at hands for the year 2017 will have to opt directly via the annual VAT return 2017 (year 2016) to be submitted within February 28, 2017. Therefore, in the form of the annual VAT return 2017, has been introduced the box “VG” to be filled out in order to exercise the option of the VAT group regime;

- as concerns the requirement in terms of time of the control, it is stated that this takes place if the shares or quotas of the controlled company have been owned for more than 50% starting from July 1 of the calendar year prior to the year of the exercise of the option (and no more starting from the beginning of the previous calendar year).

VAT applied to transport services on sea, lake, river and lagoon

In brief, starting from January 1, 2017, are subject to a VAT rate equal to 5% the “supplies of services of urban transport of people carried out through lines able to carry out transport services on sea, lake, river and lagoon”, previously considered VAT exempt with no right to deduction on the basis of the article 10, paragraph 1, no. 14), Presidential Decree no. 633/1972.

It is useful to remind that “city transport of people” means the transport carried out in the territory of a municipality or several municipalities distant no more than 50 kilometers.

As a consequence of the above legislative changes:

- the services of city transport of people carried out with taxies are exempt from VAT with no right to deduction (according to article 10, paragraph 1, no. 14), Presidential Decree no.633/1972);

- the services of city transport of people carried out via other means able to carry out transport services on sea, lake, river and lagoon are subject to a VAT rate equal to 5% (according to number 1-ter), part II-bis, table a attached to the Presidential Decree no. 633/1972);

- the services of city transport of people carried out via other lines different from the ones described at the two points above are subject toa VAT rate equal to 10% (on the basis of the number 127-novies), part III, table a attached to the Presidential Decree no. 633/1972);

- the services of extra-city transport carried out via any means are subject to a VAT rate equal to 10% (on the basis of the number 127-novies), part III, table a attached to the Presidential Decree no. 633/1972).

In this respect, generally, for transactions carried out starting from January 1, 2017, companies carrying out city transport of people via other means able to carry out transport services on sea, lake, river and lagoon can evaluate the exercise the right to the total deduction or partial deduction; however, this has to be verified/analyzed in relation to the type/types of activities carried out.

VAT reduction

Article 26 of the Presidential Decree no. 633/1972 has been changed again, by re-introducing the provisions about the recovery of VAT in case of bankruptcy procedures in force before the Stability law 2016 (Law no. 208/2015).

The provisions introduced by the Stability law 2016 (that has never became in force because it was going to be applicable only to bankruptcy procedures which would have started from December 31, 2016) had provided an important benefit for the economic operators, who, for the recovery of VAT, would not have had to wait for the unsuccessful conclusion of the bankruptcy procedures, because entitled to issue a credit note towards the debtor as from the beginning of the above mentioned procedure.

On the basis of the changes by the Budget Law, the rules in force before the Stability law 2016 are effective again through the repeal of the paragraphs 4 and 11 of the current article 26 and also including the provisions applicable to the credit notes in case of bankruptcy procedures in the paragraph 2 of the same article 26 (thus deferring, implicitly, to the practice and case law before the Stability law 2016).

In this respect, it will be necessary to wait for the unsuccessful conclusion of the bankruptcy procedures in order to recover, through a credit note, VAT not paid by the client.

In this respect, for further details, please click HERE.

Furthermore, the Budget Law at hands, by modifying article 182-ter, Royal Decree no. 267 dated March 16, 1942, linked to fiscal transaction, has recognized the principles stated by the European Court of Justice (please see the sentence C-546/14 dated April 7, 2016) on the cancellation of the VAT and of the deductions operated and not paid.

In particular, the European Court of Justice has stated that it is in line with the EU law the interpretation of article 182-ter, Royal Decree no. 267 dated March 16, 1942, when let an insolvent entrepreneur to submit to a judge a query in order to start a pre-bankruptcy procedure through which it can propose the partial payment of the VAT debt attesting, on the basis of the verification of an independent expert, that the debt could not receive a better treatment in case of failure.

On the basis of the article 182-ter, Royal Decree no. 267 dated March 16, 1942, through the proposal of pre-bankruptcy or through the agreements linked to the restoration of the debt, the debtor: can propose no more only the deferment of the payment, but also the partial payment of the VAT and of the withholding tax operated and not paid; is obliged to submit a report drafted by a professional having the requirements stated by the article 67, paragraph 3, letter d), from which it results that the satisfaction of the credit of the tax authorities, if it is favored, is not lower than the collectible one, considered the preferred collocation, on the revenue incoming in case of liquidation with reference to the market value of the goods or to the rights regarding which there is the cause of pre-emption.

Before the above law changes, the reduction of the tax debts was not permitted both for the VAT, considered its EU nature, and for the deductions operated and not paid; for those tax debts, the debtor was able to propose, via the institute of the fiscal transaction, only the deferment of the payment.

Amendments to the content of the till receipts and of the tax-receipts and introduction of a national lottery among operators opting for the e-filing of daily considerations

It has been introduced the obligation to quote the customer’s number of fiscal code in the till receipt and in the tax-receipt, only if the same customer has required it, no later than the time in which the operation has been carried out (article 3 of the regulation referred to Presidential Decree no. 696/1996). This provision shall be applied to transactions carried out from 1st January 2018.

Moreover, from 1st January 2018, natural-person taxpayers residing in the Italian territory which purchase goods and services, outside business purposes, art or profession activities, from operators which have opted for the e-filing of daily considerations (article 2, paragraph 1, legislative decree no. 127/2015), can participate to a lottery.

In order to participate to the lottery, the following conditions are required:

- the customer, upon the purchase is carried out(outside business purposes, art or profession activities), communicates his fiscal code to the operator, or requires the invoice;

- the operator transmits to the Italian tax authorities the data of the supply of goods or services according to article 2, paragraphs 3and 4, legislative decree no. 127/2015, or the data of the invoice according to article 21,paragraph 3, legislative decree no. 127/2015.

Moreover, in order to encourage the use of electronic payment instruments by customers, the likelihood of winning awards of the national lottery is increased by 20% for payments carried out by credit or debit card (referred to in article 3, paragraph 3, legislative decree no. 127/2015) compared to cash payments.

Moreover, it is provided that waiting for the actual adoption of the above rules, from 1st March 2017, on an experimental basis, of the above mentioned “national lottery” limited to the purchases of goods or services:

- outside business purpose, art or profession activities from natural-person tax payers residing in the Italian territory;

- via instruments which allow to pay with debit or credit card referred to in article 2, paragraph3, legislative decree no. 127/2015.

However, a regulation providing the technical arrangements referred to the above, will have to be issued within 60 days from the publication of the Budget Law in the Official Gazette.

Safeguard clause

The Budget law 2017, in the case budget’s goals have not been reached, provides for:

the increase of the standard VAT rate, currently at 22%:

to 25% from 1st January 2018;

to 25,9% from 1st January 2019;

the postponement to 1st January 2019 of the increase to 13% of the reduced VAT rate, currently stands at 10%.

Tax Decree linked to 2017 Budget Law: corporate income tax news

It is convenient to provide below with a summary of the main changes introduced by Law Decree October 22, 2016, no. 193, converted into Law December 1, 2016, no. 225 (published in the Official Gazette on December 2, 2016, no. 282).

Tax payment deadline

The deadlines for payment of the balance and the first advance IRES and IRAP, has been postponed at the last day of the sixth month following the end of FY. Thus for example for subjects with the fiscal year coincident with the calendar year the deadline is postponed to June 30 instead of 16 June. It is unchanged the possibility to postpone the payment of a 30-day period with the increase of 0.4%.

Integrative tax return “in favor” of tax payers

Has been introduced the possibility to file an integrative tax return in favor of tax payers within the deadlines of tax assessment.

Please note that the integrative tax return in favor of tax payers is filed in order to correct errors or omissions that determined a higher income or a higher tax liability or a lower tax credit.

Depending on the timing of the filing of the integrative return (i.e. within/over the filing of the return of the following fiscal year) different modalities to use the tax credit should be considered.

As regards VAT, it should be clarified the coordination between the new deadlines for the submission of the VAT returns in favor of the taxpayers and the one in order to deduct input VAT (art. 19, Presidential Decree no. 633/1972).

Option for special tax regimes

From FY 2017 onwards is stated the automatic renewal for the following special regimes provided by the Italian tax rules:

Fiscal transparency;

Domestic tax consolidation;

Worldwide tax consolidation.

For example, expired the election for the three years period for the Domestic tax consolidation, the latter is automatically renewed for another period, unless an express waiver.

Settlement of the tax bills

It has been granted the possibility to settle the tax bills issued for FYs 2000-2016 by the Collector Agents without disbursement of the relevant penalties and interests for late payment. Taxpayers willing to apply the settlement must file a specific claim by March 31, 2017, withdrawing the related litigation. Collector Agents will communicate the amount to be paid by the taxpayers by May 31, 2017.

Tax Decree linked to 2017 Budget Law: VAT news

New quarterly communications of data of invoices issued and received

VAT taxable persons, instead of the submission of the so-called “comunicazione polivalente”, starting from 2017 have to submit to the tax authorities, on a quarterly basis, a detailed list of the invoices issued and received and the communication of periodic VAT balances.

In particular, art. 21 of the Law Decree no. 78/2010 has been rewritten and now is entitled “Comunicazione dei dati delle fatture emesse e ricevute”. The new version of the above-mentioned article establishes the obligation for taxable persons to communicate on a quarterly basis to the tax authorities the data of all the invoices issued during the relevant quarter and all the invoices received and registered in the VAT ledgers, including customs bills of import, as well as the related credit notes.

In general, the tax provision states that the communication must be transmitted electronically to the tax authorities within the last day of the second month following each quarter.

It should be pointed out that, during the conversion of the draft of the Decree Law some amendments have been provided for deadlines of the communications at hand. In particular, the communication concerning the second quarter has to be submitted within the 16 September of the relevant year, while the one related to the last quarter of the year has to be submitted within the end of February of the following relevant year.

Moreover, taking into account a forthcoming Decree (also known as “Decreto Milleproroghe”) which is going to amend the abovementioned Decree Law no. 193/2016, only with reference to year 2017, the communication of the first half of FY 2017 is due within 18 September 2017 (considering that 16 September is Saturday) and the second half will be due by the end of February 2018. As a consequence, on one hand, the taxpayer has to submit only two communications for 2017, while, on the other hand, starting from 2018, the taxpayer will be obliged to submit four communications (i.e. one each quarter). It is useful to highlight in the table below the first three deadlines related to the VAT fulfillments at hand:

Moreover, the tax provision provides that the data must be sent in analytical form through a process established by a further act of the tax authorities, including at least the following items:

- the identification data of the parties involved in the transaction;

- date and number of the invoice;

- the taxable basis, the VAT rate applied and the related VAT;

- the type of Transaction.

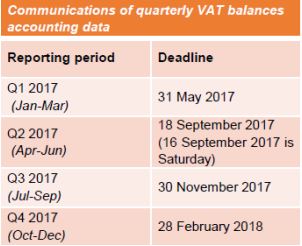

New quarterly communications of VAT balances

The Decree introduces the new article 21-bis entitled “Comunicazioni dei dati delle liquidazioni periodiche I.V.A.” in the Law Decree no. 78/2010. This article provides for the obligation to submit, with the same quarterly periodicity and the same deadline of the above-mentioned communication, the summary of the periodic VAT balances accounting data (also in case the VAT balances results in a credit balance). The operative procedure will be defined by a further act of the tax authorities. For this particular tax obligation, based on the wording of the Decree, it is not clear whether the communication of the periodic VAT balances, related to the first half of 2017, is postponed to 25 July 2017 (as provided for quarterly communications of data of invoices issued and received), therefore it might be useful if Italian tax authorities clarify this point.

For sake of clarity, with reference to year 2017, we highlight here below the deadlines related to this new VAT obligation:

Having received the data through the abovementioned communications, the tax authorities will evaluate the consistency of the data reported by the taxpayer with the tax payments carried out.

Applicable penalties

In order to make more effective both the communications, the legislature has also intervened in relation to penalties by introducing paragraph 2-bis and 2-ter in the art. 11, of Legislative Decree no. 471/1997 which provides for a penalty of 2 euro for omitted or erroneous communication of the data of each invoice, up to a maximum of 1,000 euro. In the event that the taxpayer submit the previously omitted communication (or he submit an amendment of the already previously filed communication) within next 15 days after the official deadline, penalties will be reduced by half. Basing on the wording of the Decree, the possibility to apply for the so-called “cumulo giuridico” according to art. 12 of Legislative Decree no. 472/1997 is denied.

Moreover, it is provided for a penalty from 500 to 2,000 euro for omitted, incomplete or inaccurate communication of periodic VAT settlements. As provided for the other communication, also for the communications of quarterly VAT balances the reduction by half is envisaged, in case the taxpayer will submit the previously omitted communication or he submit an amendment of the already previously filed communication.

Tax credit for the technological upgrade of ERP systems

For the necessary technological upgrade of ERP systems, it is recognized a one-off tax credit of 100 euro, to be used by offsetting it with other taxes from 2018, for the subjects who have account in the previous year a turnover not exceeding 50,000 euro. This one-off tax credit is recognized also for the taxpayer which adopts the optional regime related to the electronic submission of the e-invoices and relevant data pursuant to article 1(3), Italian Legislative Decree no. 127/2015 (for further clarifications we refer to our tax news alert dated 14 November 2016).

An additional tax credit of 50 euro is granted to those taxpayers, who send invoice data in the way prescribed by the art. 21 of Law Decree no. 78/2010, as well as, where applicable, who exercised the option provided for in art. 2, paragraph 1, of Legislative Decree no. 127/2015 (i.e. the “electronic communication of the daily considerations”).

These tax credits are neither relevant for income tax purposes nor for the value of production for the regional tax purposes.

Abolished VAT compliance obligations

Starting from January 1st 2017, as a result of the new requirements, the following fulfillments will be abolished:

- The so called “black list” communication (there is no need to submit it also with reference to 2016);

- Communications of the data of the lease agreements entered into by leasing companies according to art. 7, paragraph 12, Presidential Decree no. 605/73;

- Periodic communications of the purchases from San Marino taxable persons pursuant to article 16(c) Ministry of Finance’s Decree dated 24 December 1993.

Instrastat return, related to the purchases of goods and acquisitions of services will be due also for FY 2017. Starting from FY 2018, there will be a reduction of the information to be provided to Italian tax authorities (in relation to the arrival side of goods). Finally, the Intrastat return related to acquisition of services from other EU taxable persons will no longer be due in FY 2018.

Deadline for the annual VAT return

The Decree provides also the postponement until April 30 of the obligation of submission of the annual VAT return with reference to 2017 and subsequent years, while there are no changes for VAT return in relation to 2016, whose deadline remains February 28, 2017.

News about VAT credit refund procedure

The Decree, modifying article 38-bis, paragraph 3 and 4, Italian Presidential Decree no. 633/72, increases up to 30,000.00 euro (in relation to the previous threshold of 15,000.00 euro) the threshold below which the annual and quarterly VAT returns can be submitted, in order to claim the VAT credit, without following any particular formalities.

On the contrary, if the claimant want to ask for the refund of a VAT credit which is above the new threshold of 30,000.00 euro, on the contrary, the execution of the refund will be subjected to the following rules:

- for taxpayers in general, the so-called “vistodi conformità” (or the alternative sign of the audit body) should be affixed on the annual or quarterly VAT return and a specific self-declaration, about the equity/revenues conditions of the taxpayer, should be submitted to Italian Tax Authorities;

- Submit a specific guarantee in favor of Italian tax authorities, for certain taxpayers listed under article 38-bis, paragraph 4, Italian Presidential Decree no. 633/72 (e.g. taxpayers which have received a tax assessment in last two years, provided particular conditions are met; taxpayers which exercise business activity for no more than two years) or for certain subjects which have not affix the so-called “visto di conformità” on the VAT returns or they have not submitted the self-declaration concerning the equity/revenues conditions of the taxpayer.

The threshold at issue should be referred to all the returns submitted by the taxpayer during each calendar year and shall not be referred to each single return.

On the contrary, the threshold in order to carry out the offset with other tax and social contribution without affixing the so called “vistodi conformità”, or the subscription of the board of statutory auditors, remains 15,000 Euro.

Simplification concerning e-archiving for certain transactions

In addition, for the transactions relevant for Italian VAT purposes, the e-invoices and other electronic documents, submitted through the Interchange System and stored by tax authorities, will replace the archiving obligation provided for article 3 of Ministry of Finance’s Decree dated 17 June 2014 (see article 4, paragraph 3, of the Decree). The timeframe and the relevant technical procedure will be regulated through a proper act of the Italian tax authorities’ Director.

Transition regime of the e-submission of the daily considerations related to the entities operating in large retailers market

With reference to the business which operates in the large retailers market, the option (exercised within 31 December 2016) to submit the daily considerations pursuant to article 1, paragraph from 429 to 432 of Italian Law no. 311/2004 shall remain valid until 31 December 2017, even if this regime was repealed by Italian Legislative Decree no. 127/2015 with effect from 1 January 2017.

E-invoicing for tax free shopping

Starting from 1st January 2018, article 4-bis of the Decree provide for, in relation to the supply of goods, carried out to private person domiciled or resident outside the European Union, pursuant to the procedure provided for article 38-quarter, Italian Presidential Decree no. 633/72, the invoice must be issued via electronic means. This provision, in order to ensure the full interoperability between the e-invoicing system and the OTELLO system and to allow the fully functioning of this system at national level, refers to a further act which will be published by both Italian Customs and Tax Authorities together.

Changes concerning VAT warehouse provisions

With effective date April 1, 2017, significant changes will be introduced in relation to the use of the VAT warehouse and the way to account for VAT following the withdrawal of the goods.

The legislative changes provided for by the Decree, which amended the relevant legislation (reference is made to article 50bis, Italian Decree Law no. 331/93) can be summarized as follows:

- the difference between domestic sales with introduction into the VAT warehouse to non-established taxpayers (with EU VAT number) and domestic sales with introduction into the VAT warehouse to a taxpayer established in Italy will be no longer applicable. In other words it would be possible to carry out domestic sales with introduction into the VAT warehouse (and, as a consequence, to defer VAT payment) to any taxpayer, regardless its own Country of establishment, VAT number and disregarding the nature (i.e. commodity code) of the goods to be introduced;

- Italian VAT due upon the withdrawal of the goods from the VAT warehouse that follows a local supply of goods with introduction in such a VAT warehouse, in order to carry out a subsequent sale in the Italian territory, will be no longer accounted through the reverse charge mechanism. In particular, VAT warehouse keeper, in the name and on behalf of the taxpayer that withdraws the goods, will have to pay the VAT due on those goods to be withdrawn. This payment could not be offset with credits of other taxes (i.e. it will be not possible to apply for the so called “compensazione orizzontale”) and must be executed within the 16th day of the month following the withdrawal of such goods. In order to exercise the right to deduct, the taxpayer that withdraws the goods will have to issue a self-invoice to be registered only in the VAT purchases ledger. In particular:

- the VAT warehouse keeper will be jointly and severally liable for VAT payments with the taxpayer that withdraws the goods;

- those taxpayers that qualify as “usual exporters” will have the right to withdraw from the VAT warehouse without VAT (up to the amount of the available plafond), provided that a proper declaration of intent (i.e. “dichiarazionedi intento”) is submitted to the Italian tax authorities.

- in relation to the applicable penalties, in case of omitted or late VAT payment, art. 13 of Legislative Decree. n. 471/1997 will be applied (from 1% to 30% of VAT, on the basis of the days of delay), while in the case of withdrawal with the use of the “plafond”, in case the relevant conditions to apply for that simplification are not met, the penalty provided for by art. 7, paragraph 4, of the Decree will apply (i.e. from 100% to 200% of the VAT). For this last penalty, only the taxpayer withdrawing the goods will be liable before the Italian tax authorities.

- Italian VAT due upon the withdrawal of the goods from the VAT warehouse that follows an importation of goods with introduction in such a VAT warehouse, in order to carry out a subsequent sale in the Italian territory, will be accounted through the reverse charge mechanism, upon submission of a financial guarantee. Relevant practicalities related to the financial guarantee will be defined through a future Decree of the Ministry of finance. Such a provision, that is very similar to the one currently in place, has a lack of coordination with the provision concerning import of goods with introduction into a VAT warehouse. In this respect, further clarifications are expected. It shall be noted that in the interim period before the issuance of the above-mentioned Decree, VAT will be due according to the procedure described above.

- In case of introduction of goods into a VAT warehouse as a consequence of an intra-Community purchase, it seems that there are no changes to the current provision, as well as in respect of the calculation of the relevant taxable basis.

- The above mentioned provisions are aimed to contrast tax evasion. In this sense, it is possible to find the rationale underlying the provision that require the VAT warehouse keeper (that is subject to the customs authorities control) to pay VAT on those withdrawal following a local supply of goods with introduction into the VAT warehouse.

- However, they imply that economic operators should reconsider the use of the VAT warehouse. Indeed, the “cash-out” due to VAT payments (either at the time of importations for the interim period or at the time of domestic purchases) is only deferred at the time of withdrawal and not eliminated at all (in case goods are sold in Italy and the taxpayer that withdraws the latter does not use the so-called plafond for usual exporters).

If you have any questions in that regard, please do not hesitate to contact Luca Lavazza, Partner PwC Italy on +39 02 91605701 or luca.lavazza@it.pwc.com.

Bildquelle: Katharina Wieland Müller / pixelio.de