Italian VAT law provides for a number of simplifications, which might be used in order to avoid being charged with VAT or recover the input VAT incurred in a faster way compared to the refund, in particular:

Italian VAT law provides for a number of simplifications, which might be used in order to avoid being charged with VAT or recover the input VAT incurred in a faster way compared to the refund, in particular:

- ‘Usual exporter’ relief;

- Italian VAT grouping;

- VAT warehouse;

- Imports in the name and on behalf.

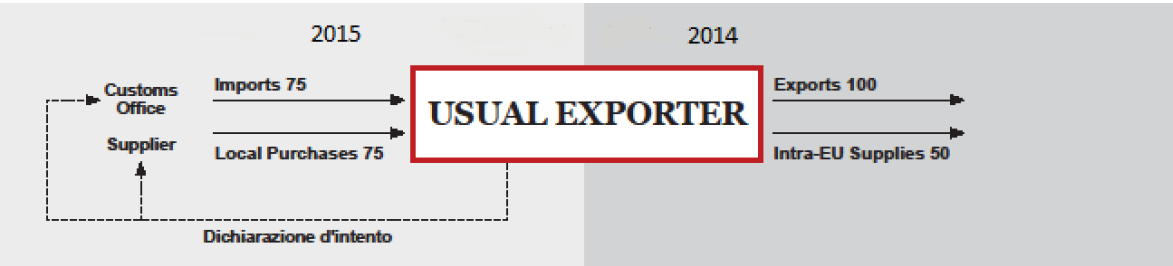

‘Usual exporter’ relief

Conditions / how does it work?

Taxable person qualify as ‘usual exporter’ when, in the previous calendar year or in the previous 12 months, carried out qualified exempt supplies for an amount higher than 10% of their Italian turnover (so called ‘plafond’).

- ‘Usual exporters’ can purchase goods and services asking the suppliers not to charge VAT up to the limit of the previous year ‘plafond’.

- ‘Usual exporters’ can ask to the customs office not to apply VAT on imports up to the limit of the previous year ‘plafond’.

Pros & Cons

Pros

- It is immediately applicable (provided that the activity has been carried out for at least the remaining part of a calendar year or 12 months);

- The costs in order to put this solution in place are low.

Cons

- The amount of qualified exempt supplies could be not enough to reduce to zero the input VAT incurred;

- The VAT credit is shifted to the supplier (in case of local purchases).

Italian VAT grouping

Conditions

- Companies are deemed to be controlled in case their stocks are owned for more than 50% as from the beginning of the calendar year preceding the one in which the group applies for the simplification.

- VAT group must contain the controlling company although there is no requirement to include all eligible controlled companies.

- EU companies VAT registered in Italy can take part to the procedure.

- VAT group application has to be submitted by 16 February and is valid for the relevant year. The option has to be renewed on a yearly basis.

How does it work?

- Input and output VAT of the companies belonging to the group can be offset at the group level.

- VAT credits offset at group level must be guaranteed (exceptions exist).

- VAT credit from previous fiscal years cannot be offset against the VAT debt of the years in which the companies apply for the VAT grouping.

- Companies of the group maintain their full independency as single taxable persons.

- Intercompany transactions are subject to the ordinary Italian VAT rules.

Pros & Cons

Pros

- This solution is generally effective.

Cons

- Not applicable to companies established outside the EU;

- Generally, it takes some time to start the simplification;

- Foreign parent companies might be required to register for VAT purposes in Italy;

- Guarantee costs (if any);

- Compliance costs.

VAT warehouse

Conditions

- VAT warehouses are physical places under the customs authorities’ control.

- Transactions carried out in connection to VAT warehouses are subject to the common VAT obligations.

- A guarantee is requested at the time the goods are customs cleared and introduced in the VAT warehouse.

- Certain requirements have to be met in order to manage a VAT warehouse.

- VAT warehouse keepers have to keep specific accountings for the goods placed in the warehouse.

How does it work?

- The following transactions can be carried out with VAT suspended:

- Introduction into the warehouse, in case of:

- Goods put into free circulation (imports);

- Local supplies of goods to taxable persons in a Member State other than Italy;

- Others.

- While the goods are stored in the warehouse:

- supplies of goods and services.

- Withdrawn from the warehouse, in case of:

- Intra-EU supplies;

- Exports.

- Transfer to other VAT warehouses.

Reverse charge applies in case goods are withdrawn in the Italian territory.

Pros & Cons (In case the warehouse is run by a third party)

Pros

- It is immediately applicable;

- This solution is generally effective in case of goods.

Cons

- Guarantee costs in case of imports;

- Logistic costs.

Pros & Cons (In case the warehouse is run by the taxpayer)

Pros

- This solution is generally effective in case of goods.

Cons

- Guarantee costs in case of imports;

- Compliance costs;

- Provided the required conditions are met, a period between 3 and 6 months should be considered in order to obtain the authorization to run a VAT warehouse;

- Abusive behavior might be challenged in case the VAT warehouse is used only for VAT benefit.

Imports in the name and on behalf

How does it works

- Taxpayers can import goods on behalf of other taxable persons acting as importer of records at the customs office.

- The importer of records (even if does not own the goods) is entitled to deduct import VAT, if the following requirements are met:

- It registers the customs declaration in the purchases ledger;

- The goods are imported for its business purposes

Pros & Cons

Pros

- It is immediately applicable;

- The costs in order to put this solution in place are low.

Cons

- The VAT credit is shifted to the importer.

For further details please contact our specialist Luca Lavazza on +39 02 91605701 or by mail luca.lavazza@it.pwc.com